Deep Inventory Management

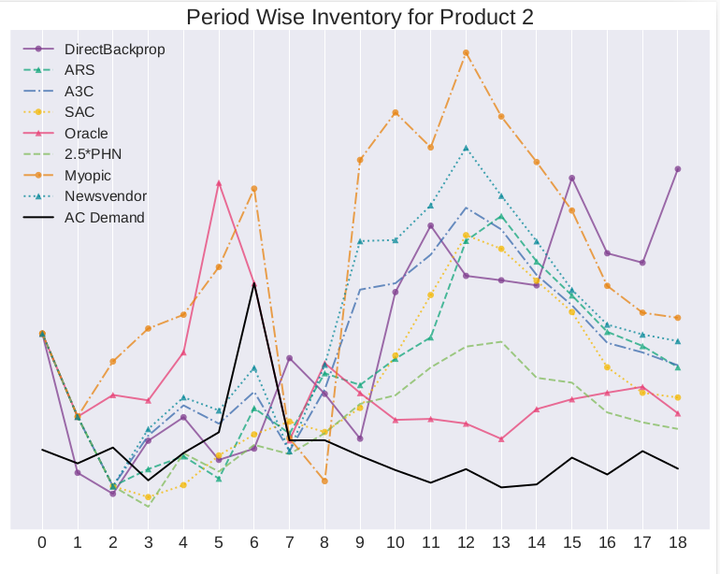

Inventory levels under different RL and baseline policies for a single product

Inventory levels under different RL and baseline policies for a single product

Abstract

This work provides a Deep Reinforcement Learning approach to solving a periodic review inventory control system with stochastic vendor lead times, lost sales, correlated demand, and price matching. While this dynamic program has historically been considered intractable, our results show that several policy learning approaches are competitive with or outperform classical methods. In order to train these algorithms, we develop novel techniques to convert historical data into a simulator. On the theoretical side, we present learnability results on a subclass of inventory control problems, where we provide a provable reduction of the reinforcement learning problem to that of supervised learning. On the algorithmic side, we present a model-based reinforcement learning procedure (Direct Backprop) to solve the periodic review inventory control problem by constructing a differentiable simulator. Under a variety of metrics Direct Backprop outperforms model-free RL and newsvendor baselines, in both simulations and real-world deployments.